There is a lot of encouraging news around giving confidence that the outlook for the economy is positive for at least the next two years or so. The worst of the pandemic seems to be behind us and the road has been cleared for people to start returning to work in offices again. Developer confidence should be boosted as scenarios of deserted offices abate, and demand from the hospitality and leisure sectors is sure to follow.

UK business investment is forecast to rebound strongly this year, helped by a government tax incentive – the super-deduction – and asset owners dealing with a backlog of needed upgrades. UK companies are estimated to have cash reserves that have swollen by over £140bn since the pandemic started, so money is there to fund it.

The optimism is supported by forecasts from the Office for Budget Responsibility and the Bank of England. The Confederation of British Industry says the share of businesses planning to invest in plant and machinery is at its highest for 33 years. Caveats can also be found – many bets might be off if a deadlier or more infectious COVID-19 variant emerges for example. But the balance of opinion among forecasters is optimistic.

This is reflected in steel construction sector forecasts, with market researchers Construction Markets forecasting strong growth in 2022 and 2023, to take output of constructional steelwork above 900,000 tonnes for the first time since the financial crisis of 2008 (see News). Growth was strong in 2021, rising by almost 17% to 803,000 tonnes, and another 10% should be achieved this year before settling down to around 2% growth in 2023.

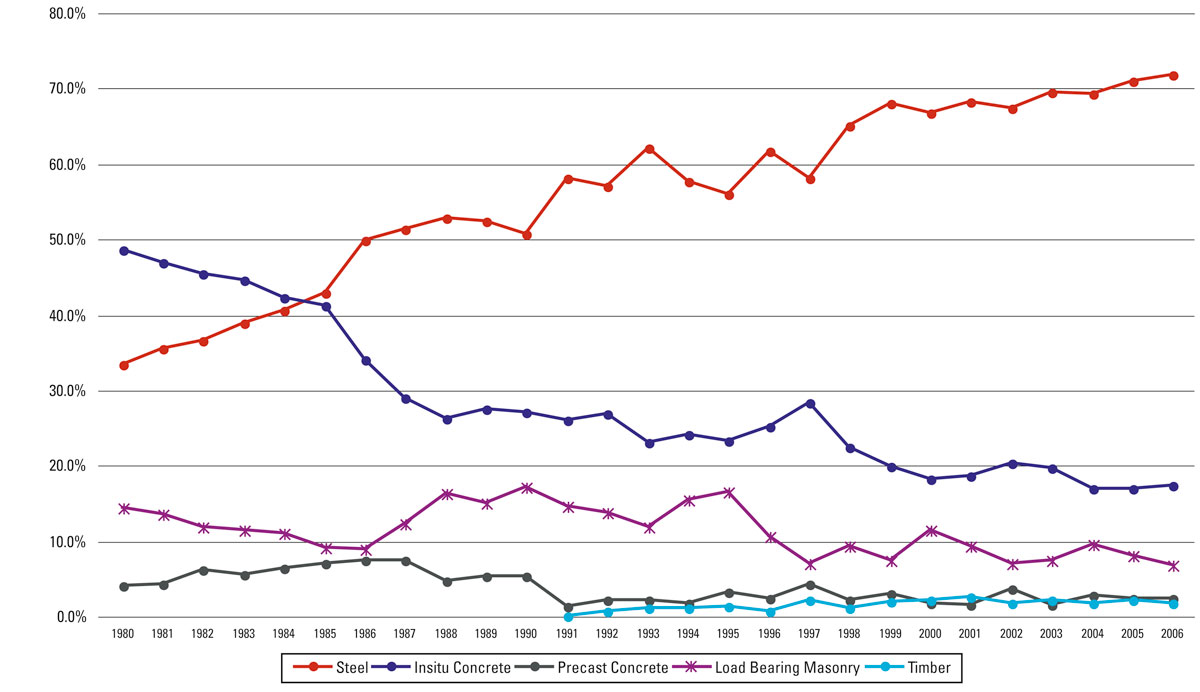

The accompanying Market Shares Survey from Construction Markets – the most comprehensive independently-produced survey of its type, in a series stretching back to 1980 – shows that steel increased market share significantly in key sectors like single storey buildings and multi-storey commercial developments. Those markets were themselves growing, with single storey industrial buildings demand growing by over 14%.

Government investment in healthcare, education and low carbon energy production are among factors likely to support demand for steel over the next few years.

Last year’s performance was achieved against a harsh background of global factors including the pandemic, disrupted supply chains, and rising raw materials prices that hit all construction materials. The spotlight was turned on the implications for climate change of all economic activities by the COP26 event in Glasgow.

Steel was not alone in rising above the challenges, but certainly showed the strength of its supply chain, and a willingness to collaborate to find solutions and ease the path over the broad-based challenges that COVID-19 and supply disruptions threw up.

Growing market share in last year’s rising market proves that key messages about steel’s inherent sustainability and other advantages are appreciated by clients and designers of their projects. Publication of the zero-carbon Roadmap last year points the way forward for steel to play its full part in combatting climate change, improving carbon related performance year by year at a pace to support government targets.

In an inflationary environment steel still provides the most cost-effective framing solutions, and has a supply chain proven to be resilient in the face of the unexpected. But if the forecasts prove accurate, it will be good to get back to rising to ‘normal’ challenges.

Market shares and demand outlook strengthen

There is a lot of encouraging news around giving confidence that the outlook for the economy is positive for at least the next two years or so. The worst of the pandemic seems to be behind us and the road has been cleared for people to start returning to work in offices again. Developer confidence should be boosted as scenarios of deserted offices abate, and demand from the hospitality and leisure sectors is sure to follow.

UK business investment is forecast to rebound strongly this year, helped by a government tax incentive – the super-deduction – and asset owners dealing with a backlog of needed upgrades. UK companies are estimated to have cash reserves that have swollen by over £140bn since the pandemic started, so money is there to fund it.

The optimism is supported by forecasts from the Office for Budget Responsibility and the Bank of England. The Confederation of British Industry says the share of businesses planning to invest in plant and machinery is at its highest for 33 years. Caveats can also be found – many bets might be off if a deadlier or more infectious COVID-19 variant emerges for example. But the balance of opinion among forecasters is optimistic.

This is reflected in steel construction sector forecasts, with market researchers Construction Markets forecasting strong growth in 2022 and 2023, to take output of constructional steelwork above 900,000 tonnes for the first time since the financial crisis of 2008 (see News). Growth was strong in 2021, rising by almost 17% to 803,000 tonnes, and another 10% should be achieved this year before settling down to around 2% growth in 2023.

The accompanying Market Shares Survey from Construction Markets – the most comprehensive independently-produced survey of its type, in a series stretching back to 1980 – shows that steel increased market share significantly in key sectors like single storey buildings and multi-storey commercial developments. Those markets were themselves growing, with single storey industrial buildings demand growing by over 14%.

Government investment in healthcare, education and low carbon energy production are among factors likely to support demand for steel over the next few years.

Last year’s performance was achieved against a harsh background of global factors including the pandemic, disrupted supply chains, and rising raw materials prices that hit all construction materials. The spotlight was turned on the implications for climate change of all economic activities by the COP26 event in Glasgow.

Steel was not alone in rising above the challenges, but certainly showed the strength of its supply chain, and a willingness to collaborate to find solutions and ease the path over the broad-based challenges that COVID-19 and supply disruptions threw up.

Growing market share in last year’s rising market proves that key messages about steel’s inherent sustainability and other advantages are appreciated by clients and designers of their projects. Publication of the zero-carbon Roadmap last year points the way forward for steel to play its full part in combatting climate change, improving carbon related performance year by year at a pace to support government targets.

In an inflationary environment steel still provides the most cost-effective framing solutions, and has a supply chain proven to be resilient in the face of the unexpected. But if the forecasts prove accurate, it will be good to get back to rising to ‘normal’ challenges.